|

||

|

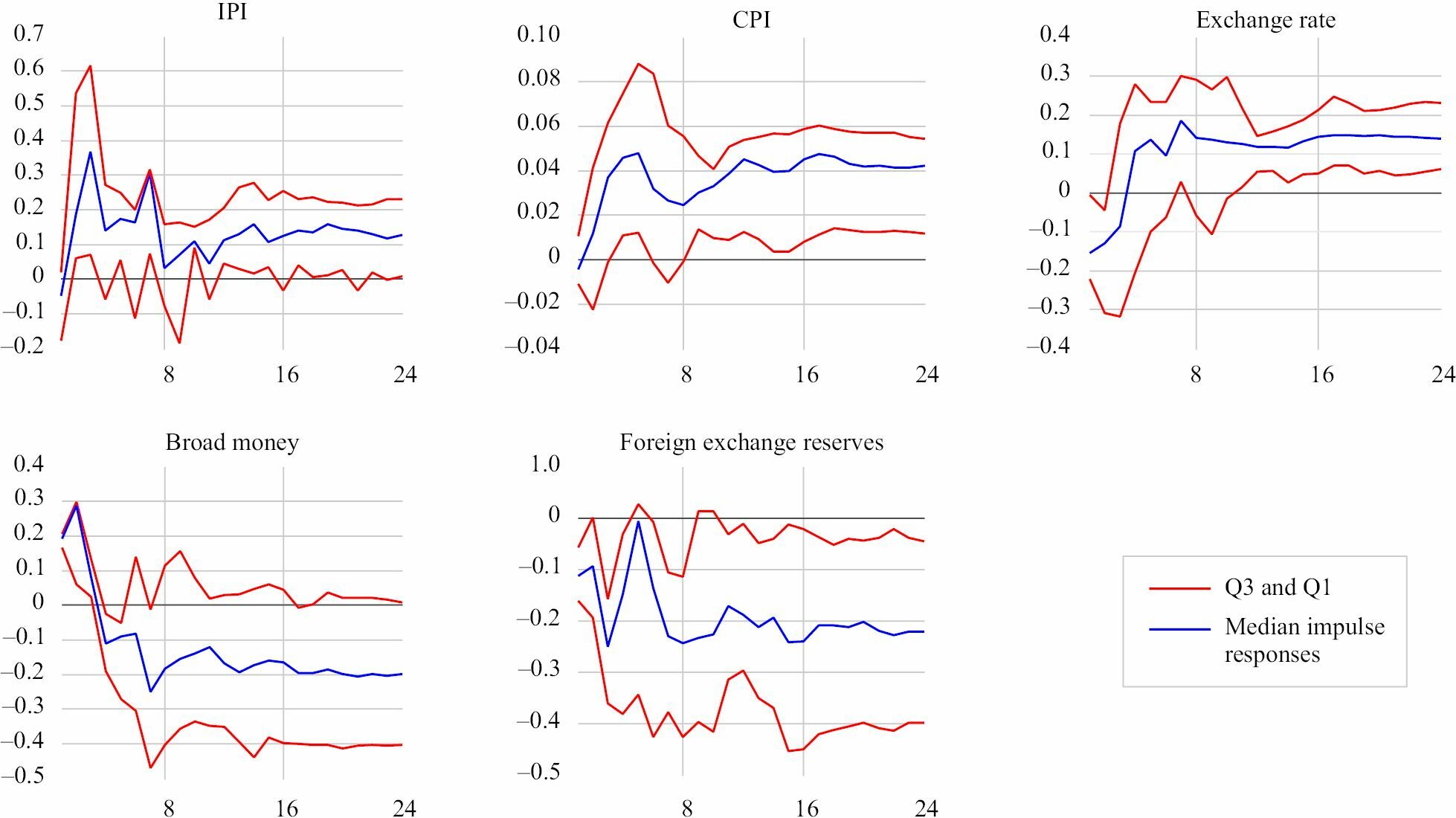

Impulse response functions to shock in US shadow rates: Latin America. Note: The figure depicts the IRFs to a one-standard deviation positive shock in US shadow rates for a monthly dataset on EMEs from Latin America. The point-wise median responses are the percentage response of macroeconomic factors due to an unanticipated positive shock in the US shadow rate over time. Source: Compiled by the author. |