|

||

|

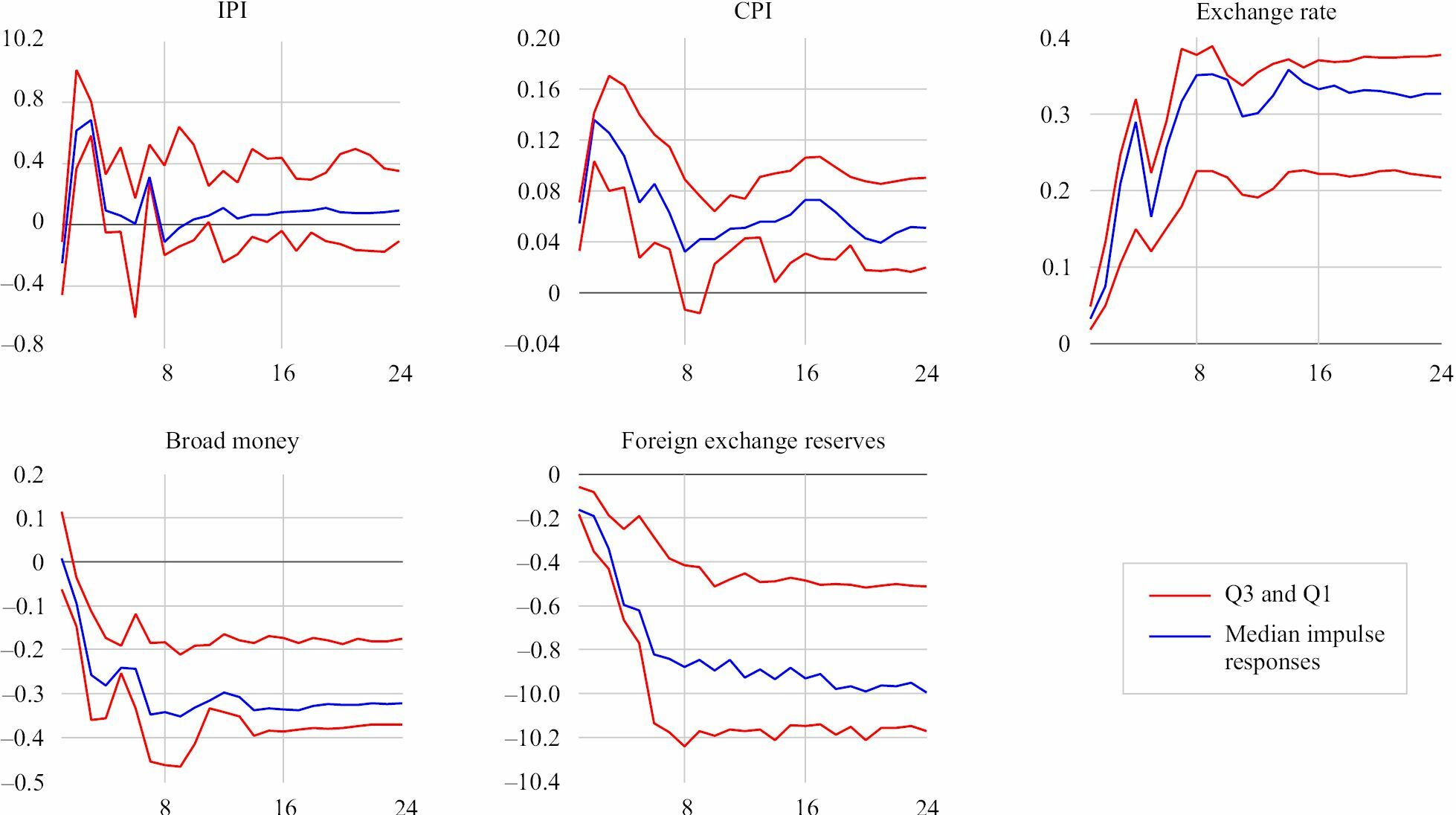

Impulse response functions to shock in US shadow rate: Asia. Note: The figure depicts the IRFs to a one-standard deviation shock in US shadow rates for the monthly dataset on EMEs from Asia. The median impulse responses represent the percentage response of an unanticipated positive shock in US shadow rate on the Asian emerging markets over time. Source: Compiled by the author. |