|

||

|

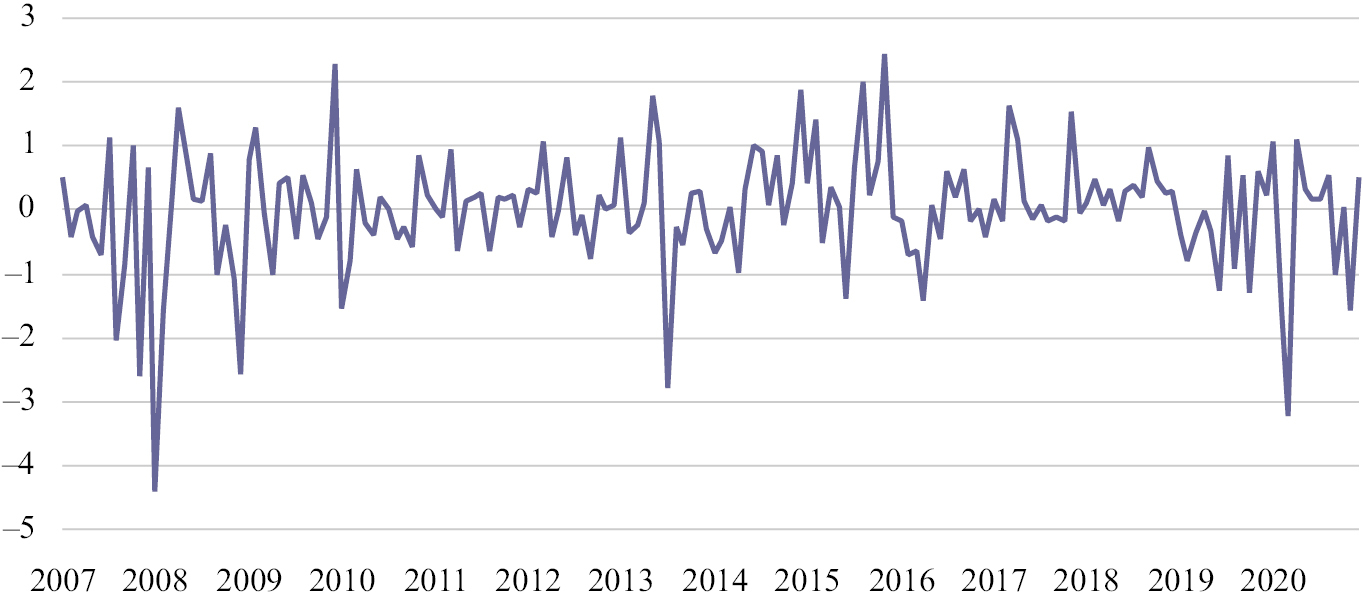

Plots the unanticipated shocks in the US shadow interest rate, 2007–2020 (%). Note: The unanticipated shocks are identified from the US SVAR model. The residuals from this model are considered as unanticipated shocks in the shadow rates. The largest contractionary shocks can be seen in 2008, depicting the quantitative easing measures. Source: Compiled by the author. |