|

||

|

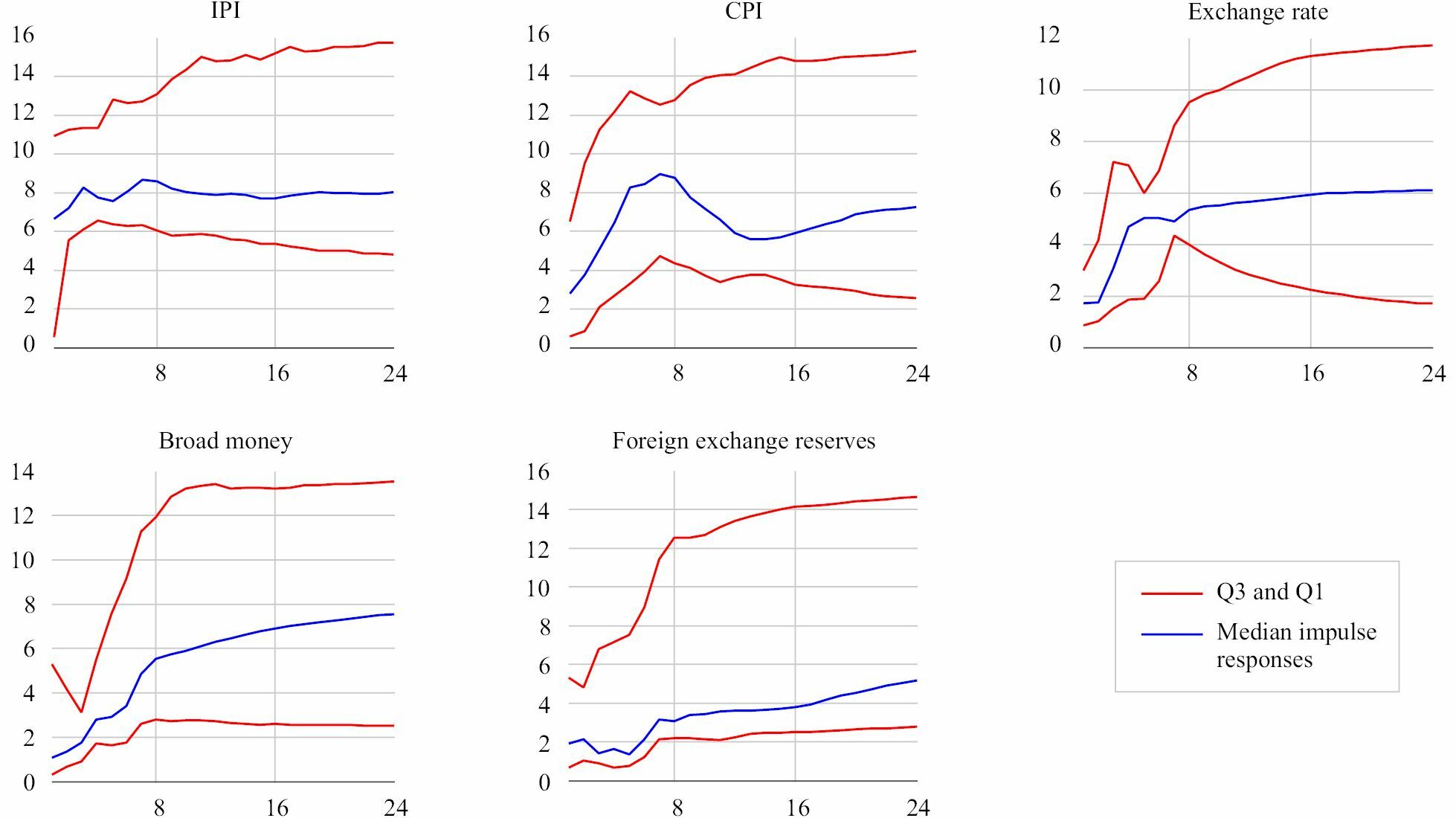

Variance decomposition forecast due to shock in US shadow rates: Europe. Note: The figure depicts the variance decomposition forecast for EMEs from Europe due to unanticipated shock in the US shadow rates. Each plot shows the percentage of median responses due to shock in the US shadow rate with interquartile range. Source: Compiled by the author. |