|

||

|

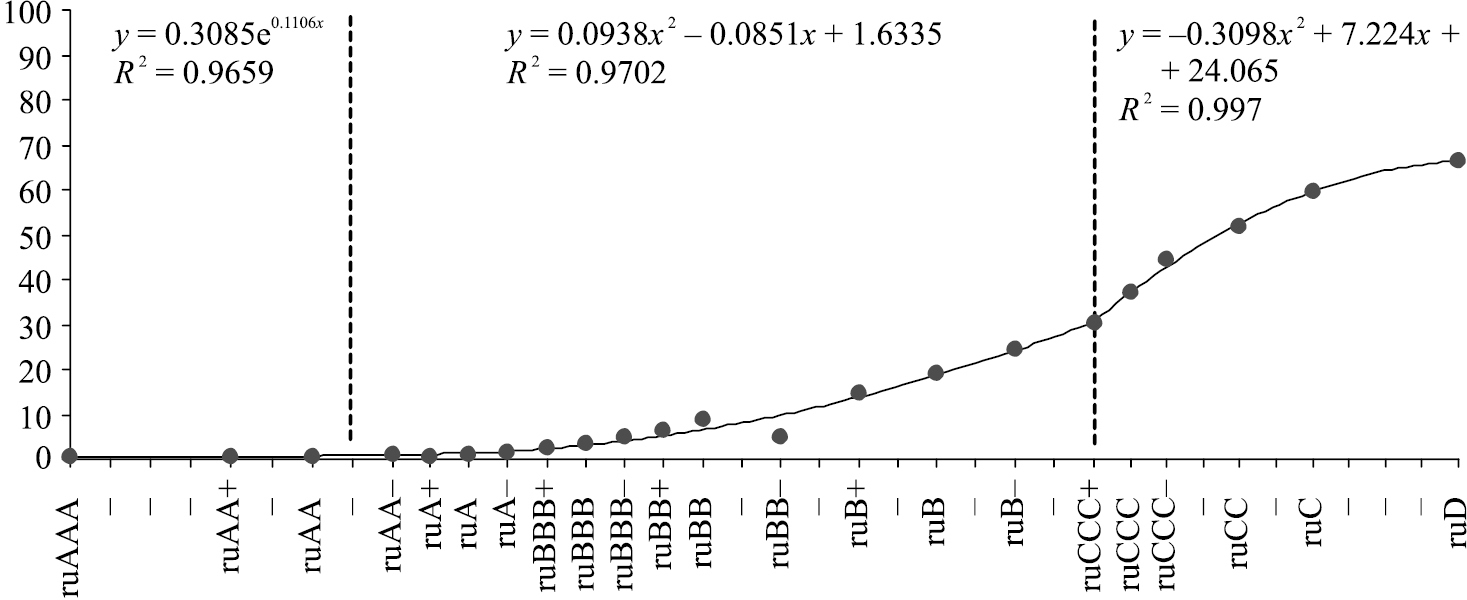

Calibration of probability default (%) and the base rating scale. Source: Authors’ calculations. |

|

||||||||

| Part of: Karminsky A, Khromova E (2018) Increase of banks’ credit risks forecasting power by the usage of the set of alternative models. Russian Journal of Economics 4(2): 155-174. https://doi.org/10.3897/j.ruje.4.27737 |